Have you ever thought of whether you have enough money to sustain your lifestyle after retirement? I think I am like most people, retirement planning is not something that I will think of when I was young till early adulthood. At my current age, even though no longer young, better to start pre-plan retirement now.

Pre-Plan Retirement: My Story

One of the enemies of retirement funds is inflation. Keeping money under the bed, in a savings account, or in fixed deposits will be eaten up by yearly inflation. If inflation is higher than the interest we earn on our investments, our money will lose value over time. Hence, pre-plan retirement by taking into account all factors is crucial.

Today, we had brunch at a normal noodle shop along Jalan Kuching. One bowl of curry noodle with chicken costs RM 13 and wan tan noodle is RM 10.50. Compared to 10 years ago, I suppose that a single bowl of noodles costs around RM 5. I really missed those days when 1 piece of roti canai was just 50 cents, but I was only at primary school at that time. 😜

Retirement is a significant milestone in our lives, and proper planning is necessary to ensure a comfortable and secure future. I guess nobody will want to work for money just to make ends meet after retiring. Plan and act as early as possible; time is crucial in preparing for retirement. Imagine, for easy illustration, let say we need RM 100K at age 60 to retire. Start working on the retirement fund at age 40 is much easier compared to age 50. At 40, we need to save approximately RM 416 per month for 20 years. If we start at 50, we would need to save RM 833 per month, assuming we haven’t earned any dividends or interest from investments or fixed deposits. And frankly speaking, living in a city with that amount, in my opinion, it is not going to be sufficient hence pre-plan retirement is an important aspect in our life.

I need to start taking retirement planning more seriously and put in more efforts starting today. You have been to Singapore and have meal at the food court, do you notice who are the staff that are cleaning the table, plates, etc.? Can Malaysians retire with enough money to live comfortably and cover living expenses for the rest of their lives?

For Chinese people even dying also requires substantial money for the funeral and final resting place.

Savings Only is Not Enough for Pre-Plan Retirement

In today world with inflation getting worst, saving money only under the bed, put into the saving accounts or even Fixed Deposit, we are going to lose to inflation. As of writing, the basic saving account’s interest rates per annum from one of our Malaysian bank is ranging from 0.25% to 0.30%, where by for Fixed Deposit it is ranging from 2.40% to 2.70% pa.

There are two type of inflation:

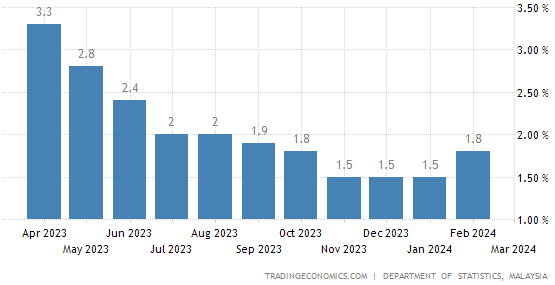

- Consumer Price Index (CPI) tracked by the government which track a fixed basket of goods and services. From the average yearly inflation rate below, what do you think? Is the actual inflation rate of the specified goods, foods and services that use same, less or more than the official inflation rate? To me, for the past 2 years, the rising of food prices is quite substantial. A bowl of noodle in the normal food court now is RM 8 to RM 9, and I always making joke on the chinese tea ice, now can costs up to RM 1. Those days, of course ages ago I think it was like 20 or 30 cents, then slowly become 50 cents.

- Lifestyle Inflation, see wiki definition below. In laymen term, it is we increase our spending when our income increased.

Lifestyle creep, also known as lifestyle inflation, is a phenomenon that occurs when as more resources are spent towards standard of living, former luxuries become perceived necessities.

Wikipedia, the free encyclopedia

There is a good article written by FMT on Inflation vs cost of living. You can read it from here.

EPF and PRS: What You Need to Know

Private retirement schemes in Malaysia are primarily managed by the Employees Provident Fund (EPF) and Private Retirement Schemes (PRS). The EPF is a mandatory retirement savings plan for Malaysian citizens and permanent residents working in the private sector, while PRS is a voluntary long-term savings and investment scheme to supplement your EPF savings. And with the introduction of KWSP Account 3 (Akaun Fleksible), what does it means for you. Do not overlook the importance of the topic of pre-plan retirement.

The question is whether the historical average return from EPF and PRS is more than yearly inflation rate or your lifestyle inflation rate? This is something we need to take note of. So pre-plan retirement must always factor in inflation rates.

Invest Our Money – Make It Work Harder

Another alternative is to invest our extra money in the US stock market. It is risky if we invest or trade based on suggestion from friends or internets without knowing how to evaluate a good company, when to enter & exit and risk management. So I choose to equip myself with the knowledge by attending Versatile Trader Program (cover both Growth Investing and Trend & Swing Trading) with Beyond Insights. You can find out more by attending their free preview on Global Investing & Trading Made Simple.